by Robby DeGraff, Manager of Product and Consumer Insights

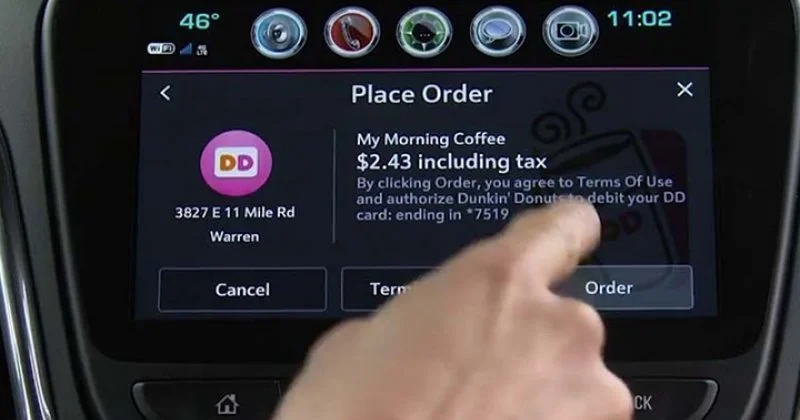

With automakers prioritizing connectivity and exploring new ways to generate revenue after the point of sale, consumers are becoming more interested in the ability to purchase items or services directly from a vehicle’s center infotainment screen. This feature isn’t necessarily “new.” Over the past decade, automakers have tried testing the waters with in-vehicle marketplaces but to the reception of little actual interest among consumers. However, recent breakthroughs in screen sizes and intuitive software with over-the-air updates, and a booming e-commerce scene have prompted automakers to give this feature another go. AutoPacific research has seen demand for the ability to purchase products, technologies, and vehicle upgrades directly from a center infotainment screen grow by 8% pts YoY. We predict that figure to continue to rise.

18% of all new vehicle intenders, and 29% of EV intenders want to use their touchscreen for transactions

When surveying new vehicle intenders, 18% of those who plan to buy a new vehicle within the next three years want the ability to purchase products, technologies, and vehicle upgrades directly from a center infotainment screen. Past research has shown younger consumers are generally more comfortable and open to connected technology in their vehicles, as well as electrification. That’s expectedly the case here, with demand peaking among those ages 30-49 before dropping sharply.

Befitting, intenders of EVs who likely anticipate spending time waiting for their vehicle to charge, want this feature the most and considerably more so than ICE intenders (+16% pts). Automakers with EVs in their lineup could benefit by providing consumers in-vehicle marketplace capabilities, since these EV intenders frequently use a vehicle’s center infotainment screen for certain activities while parked, including streaming video content, playing games, partaking in video conferencing, and browsing the internet.

Regardless of powertrain or segment, this feature could become a must-have among families, as demand was more than twice that of households without any children. From placing food orders while waiting in the school pickup line to purchasing heated rear seats while on a winter road trip, obtaining products and services conveniently through the center infotainment screen can be a reprieve for busy parents. Relevant products, services, and upgrades catered specifically to families’ needs should be readily available via an in-vehicle marketplace.

Enhancing the vehicle and ownership experience over time

Beyond common goods and services, certain features and technologies that weren’t initially offered or added to a vehicle at time of purchase can be downloaded later through an in-vehicle marketplace. These can include ADAS features, comfort amenities, and even performance-focused treats like quicker acceleration and extra range for EVs. We believe this opens the door for manufacturers to let an owner easily enhance and better their vehicle over time. Maybe you didn’t think you’d need a hands-free highway driving assist when you first drove your vehicle off the lot…but now you suddenly do because you’re road-tripping a lot. A few minutes and taps on the center touchscreen, and you’ve just upgraded your vehicle without ever stepping foot in a dealership.

Concerns and considerations to ensure seamless transactions

Earlier attempts at in-vehicle marketplaces were flawed by complicated on-screen steps, lagging connections and syncing of an owner’s payment methods, as well as a relatively small number of participating vendors. In order to ensure best practice for a consumer to purchase products, technologies, and vehicle upgrades directly from a center infotainment screen, the process must be as quick, easy, and straightforward as it would be to do so using a mobile device. Any interruption, glitches, or difficulty during an on-screen transaction would likely see the consumer immediately resorting to completing the transaction on their smartphone.

Furthermore, privacy may be a real concern for some consumers, even those open to having connected technology in their vehicle. 66% of all respondents, and 70% of those who want the ability to securely purchase products, technologies and upgrades from their vehicle’s center infotainment screen say they are concerned about their privacy due to use of various technologies. Transparency, a way to opt out of a transaction if desired, and of course security for all stored payment methods need to be guaranteed by the automaker.