by Deborah Grieb, Director of Marketing and Consumer Insights

The 2025 Consumer Electronics Show (CES) in Las Vegas was, as always, a spectacle of amazing new technological developments that boggle the mind. Of course, the AutoPacific team was on site to cover the latest automotive technology developments. There were clear themes that dominated automotive at CES, and best of all, AutoPacific’s studies, data, and services provide strong and actionable insights on all of these themes.

China:

Chinese vehicles and technology were on full display, amazing attendees with their technology, build quality, creative out-of-the-box features, and very appealing price points. In particular, the display by Zeekr, a Geely-owned cousin of Volvo and Polestar, blew atten dees’ minds, and the brand used the show to showcase not only their products, but also their global ambitions. CES served as the gateway for the booming brand to really introduce itself to industry attendees, with its introductory press conference at standing room only, followed by swarms of curious showgoers eager to sit in three of Zeekr’s products. Great Wall Motors’ display also impressed, and they are accomplished enough of an automaker that BMW uses their compact EV platform for its electric versions of the MINI Cooper and Countryman.

The threat to other automakers has been well documented, but what does the American consumer think? AutoPacific’s syndicated Future Vehicle Planner (FVP) suite of new vehicle shopper data and the studies generated from them show surprisingly high awareness and consideration for Chinese vehicles if they were sold Stateside. AutoPacific’s data on attitudes towards Chinese brands and vehicles is a crucial tool in developing strategies to meet the challenge from China head-on. Trade barriers will keep them out for only so long; the consumer has spoken, and the consumer wants Chinese vehicles. And Chinese automakers will figure out, sooner or later, how to gain entry into the U.S. market.

Autonomous and ADAS Features:

Automotive inches ever closer to full autonomous driving, and the advances seen at CES this year were no doubt beyond impressive. But ultimately, what does the consumer think about autonomous driving and semi-autonomous ADAS features? AutoPacific’s Future Attribute Demand Study (FADS) asks the new vehicle shopper directly about their desire for L2 through L5 autonomy, as well as all of the ADAS features either in market or coming soon. Understanding consumer demand and their receptivity to various autonomous features is critical in building a business case for adopting these features in future vehicles.

Software Defined Vehicles:

Software Defined Vehicle (SDV) features continue to make huge advancements, and there was no shortage of new SDV features and ideas shown at CES this year. Of course, SDVs often entail additional cost to the consumer after acquiring their new vehicle, and there is a fine line between perceiving value in software-defined features and feeling nickel-and-dimed. AutoPacific’s Future Attribute Demand Study (FADS) measures demand for a multitude of software-defined features with post-purchase costs (such as monthly subscription fees) clearly indicated to the survey taker. As SDVs are clearly a staple of the future automotive landscape, understanding consumer demand for these features at their likely price points is critically important in developing software-defined offerings to future new vehicle consumers that will delight and provide value.

AI:

Of course, virtually nothing can be discussed today without some mention of AI. And certainly, AI is emerging everywhere in automotive, from autonomous drive features to intelligent assistants that can shape the drive experience based on the interpretation of the driver's mood, physical condition, and where they are driving to. Many of these AI-powered features are covered in the Future Attribute Demand Study’s (FADS) extensive battery of features, ranging from AI-powered voice assistants to AI-powered autonomous drive features.

Electric Vehicles:

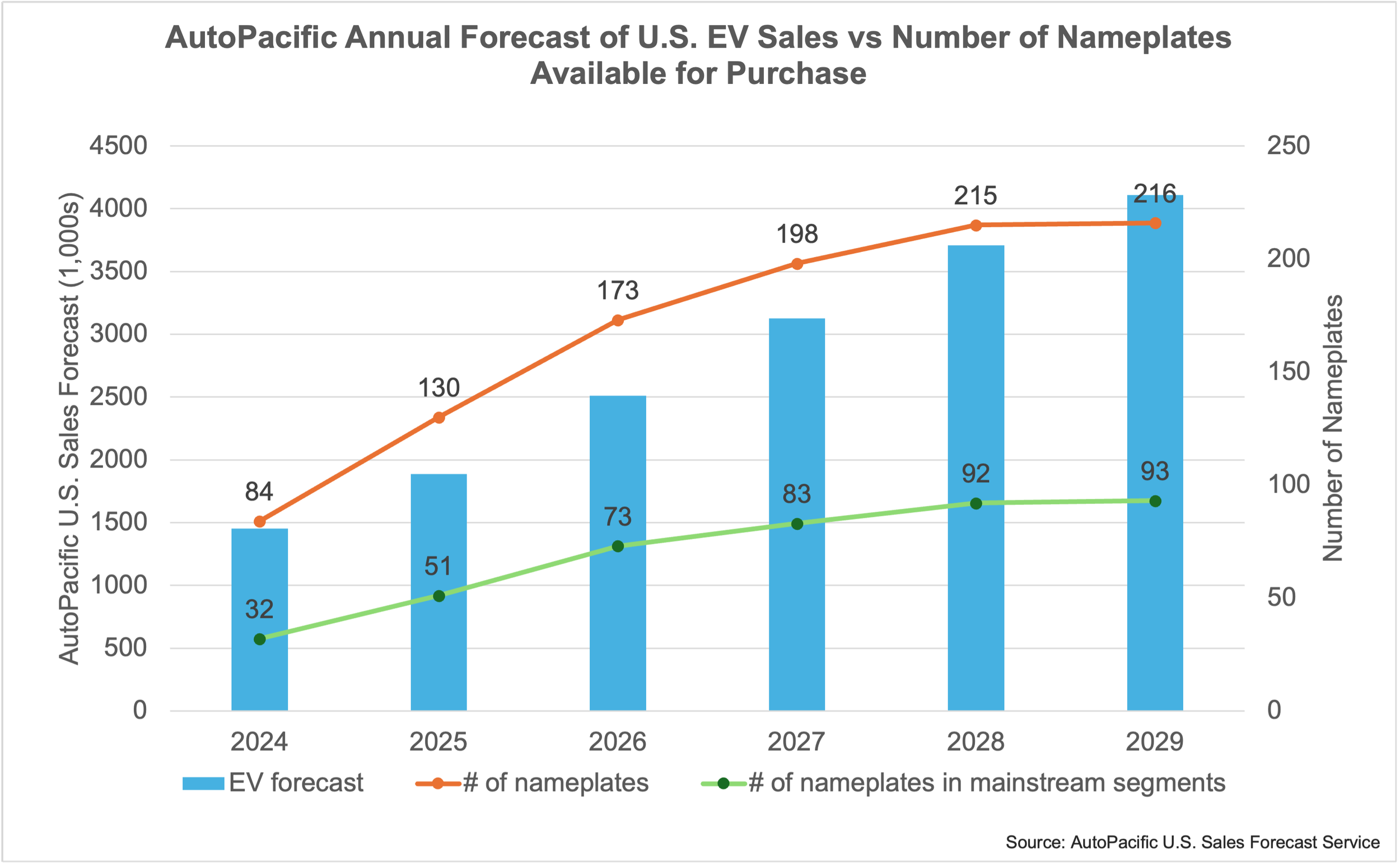

Electrification is here to stay and there was no shortage of new EV technologies from batteries to motors to full electric drive units on display. EV technology is developing fast with new battery chemistries and more efficient motors providing big improvements in range and charge times. AutoPacific’s EV Consumer Insights study thoroughly covers attitudes towards EVs, charging, range, price, and many other EV-related issues with EV owners, EV acceptors, and maybe most important, EV rejectors.

Our Industry Analysis division specializes in competitive intelligence and sales forecasting. AutoPacific’s Competitive Battleground is an online service that provides detailed vehicle product intel on every vehicle offered or soon-to-be offered in the U.S. market, including EVs. AutoPacific’s Sales Forecast Service offers detailed model-level EV, PHEV (including EREV), and hybrid forecasts, updated quarterly. These two services offer automakers with a complete view of the competitive EV market environment, both from a product perspective and future sales perspective.